CPIA - Thought Leadership

The independent voice shaping trust in UK Public Interest Entity audit

As the UK prepares for its most significant audit reforms in decades, the Centre for Public Interest Audit (CPIA), formed in July 2024, stands uniquely positioned. We bridge divides between stakeholders and the audit firms they rely on for assurance on financial reporting. Through evidence-based research and insight, the CPIA seeks to drive a better understanding of the value of audit quality. Alongside this, we advocate for proportionate and practical audit reforms for the Public Interest Entity (PIE) audit landscape.

The UK audit profession faces significant change. The long-awaited Audit Reform and Corporate Governance Bill has yet to be published for parliamentary consideration. Indications are that announcements may now slip into 2026. Expanded Public Interest Entity (PIE) definitions could bring hundreds more large companies into scope, and stakeholder confidence in audit continues to evolve.

Proportionate audit reform protects the public interest and keeps compliance practical. Done right, it strengthens trust without stifling the energy and ambition of UK business.

Dean Beale

Executive Director of the CPIA

Large corporate failures from the previous decade exposed weaknesses in audit, reporting and governance. The consequences were systemic, affecting pension holders, suppliers and communities. Since 2018, the auditing landscape has evolved, resulting in improvements in audit quality, as evidenced by the Financial Reporting Council (FRC) data demonstrating continuous progress across the largest firms. The focus now centres on sustaining this momentum.

The CPIA brings something genuinely different to this debate, being an objective voice with a mission to improve audit quality and trust.

With independence as CPIA's North Star, the organisation asks difficult questions others might avoid. We challenge both the profession and its critics with equal rigour. Most importantly, we advocate for reforms that genuinely strengthen audit quality rather than simply adding regulatory burden to businesses or the firms that audit them.

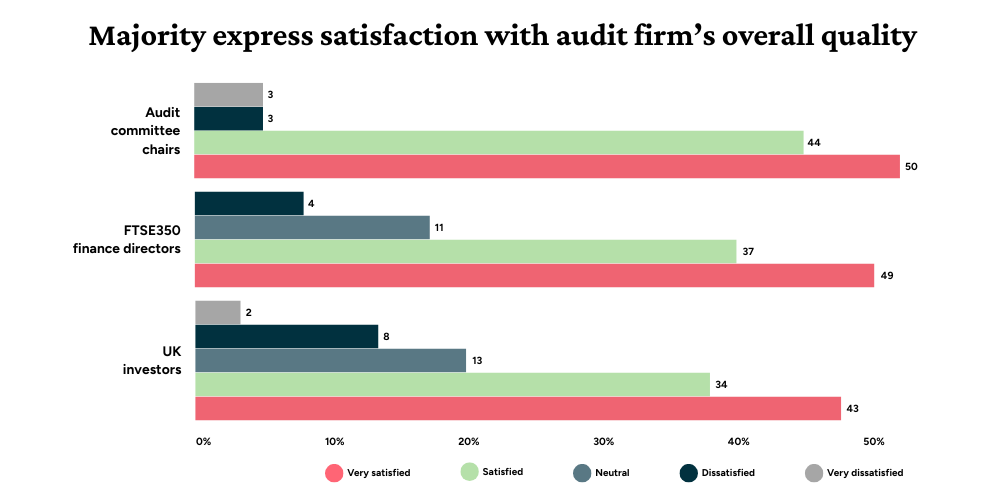

Our flagship Audit Trust Index (ATI), launched in 2024, measures and tracks perceptions of audit quality across three stakeholder groups: Investors, FTSE 350 finance directors and Audit Committee Chairs. The majority expressed satisfaction with the audit quality provided by firms:

Russell Bedford International Young Partners & Managers Conference 2023

However, our research also found areas for improvement. One in three audit committee chairs lacked confidence that auditors could spot signs of financial distress, despite recent reforms designed to address this issue. Meanwhile, 85% of FTSE 350 finance directors expressed satisfaction with audit value, yet only 59% of audit committee chairs shared this view, with 22% expressing dissatisfaction. These statistics represent potential disconnects between those commissioning audits and those relying on their outcomes. We're publishing our 2025 ATI later in November 2025, which will show how these views have evolved.

CPIA responds to these findings through targeted action. Our research lays the foundation for further insight and engagement with key stakeholder groups. Our latest roundtable with audit committee chairs navigated topical issues, such as going concern and interim cash flow complexity, with clear takeaways:

- There is a difference in usefulness between information presented in management packs, in analyst presentations, and on the face of financial statements.

- When considering fraud risk, both management and auditors play important roles in assessing the overall risk environment - beyond meeting reporting standards.

- The importance of clear disclosures is to reflect financial performance in a succinct way, and in some cases, to determine where less is more.

Our formula is simple: Research identifies challenges, stakeholder engagement develops solutions, and practical guidance drives implementation.

The Government's audit reform proposals continue to incubate with the promise of further consultation on key policies, such as expanding the PIE definition and bringing in larger private companies. The CPIA's data-driven insights can help bring objectivity to the debate.

We've launched a series of parliamentary briefings that translate complex audit issues into clear, accessible insights. Our PIE briefing notes cut through jargon to explain what being a PIE means, how the PIE audit scope differs from standard audits, and where regulatory frameworks overlap.

On a global level, much is changing in terms of philosophical views on the role of regulation. We are witnessing a real-time experiment in public policy. Views on the nature and value of regulation and assurance, on the face of it, are diverging sharply between the European Union and the United States. And in a post-Brexit UK, our approach has never been required to be more nuanced.

Baroness Margaret Ford

Chair of the CPIA

Baroness Margaret Ford

Chair of the CPIA

The market capacity for audit firms capable of conducting PIE audits remains critical. The FRC acknowledges that a more balanced market is still a considerable time away. We examine why challenger firms struggle to scale and identify the practical and regulatory barriers they face. Our strategy includes supporting new PIE auditor entrants and ensuring the market is resilient, with the right capacity and capabilities to meet future demands.

Through collaboration with similar research and policy organisations in the US and Canada, CPIA exchanges insights on global trends and market developments. As audit firms navigate evolving ownership models and private equity investment, CPIA will track how these changes affect the UK market, drawing on international experience to identify necessary guardrails.

In surveys, senior finance leaders report a shortage of talent in accounting and finance roles. We aim to build a professional community that highlights the benefits of working in audit. Our plans include a podcast series featuring seasoned PIE auditors sharing their career journeys, and forums on the opportunities and challenges of deploying AI in PIE audit.

We invite audit professionals seeking practical guidance, committee chairs wanting enhanced oversight, investors requiring clearer reporting insights, and policymakers and regulators shaping the reform agenda to the table.

Supported by our research, CPIA can help improve audit quality, build trust in audit, and, in turn, support proportionate reforms. Ultimately, we want to benefit businesses and strengthen confidence in the UK’s capital markets.

To learn more about CPIA's research, upcoming events, and how to engage with our work, visit cpia.org.uk or follow us on LinkedIn.

Main video supplied by NanoStockk/Creatas Video+ / Getty Images Plus via Getty Images

The US Context and the European Union’s Regulatory Turn

We have known for some time that prioritising sustainability-related concerns depends on individual US states and the willingness of the President to make it a focus of the political agenda. And yet, it is my impression that the real turning point in people’s perceptions had little to do with the situation on the other side of the Atlantic and everything to do with the Omnibus, the European Union’s rather dramatic U-turn.

For those who may not have followed in detail, on 26 February this year, draft proposals containing far-reaching modifications were released but still need to be adopted. As far as the Corporate Sustainability Reporting Directive (CSRD) is concerned, the key areas where we expect modifications concern the implementation timetable and the content of the reporting directive.

‘Stop the clock’ is relatively simple in nature, proposing to postpone reporting required by Wave 2 and Wave 3 companies by two years. The content proposal is a little more complex and includes four areas of focus: the overall scope of the Directive, value chain related requirements, assurance-related requirements and updates to the European Sustainability Reporting Standards (ESRS).